Rare Earth Elements and Global Geopolitics: Strategic Dominance, Supply Chain Vulnerabilities, and the Energy Transition

October 06, 2025 Rajas Purandare

Introduction -

Rare Earth Elements (REEs) comprise 17 critical minerals essential for various advanced technologies, including renewable energy systems, defence applications and consumer electronics. Their unique chemical and physical properties make them indispensable in modern industries, from electric vehicles and wind turbines to missile guidance systems and semiconductor manufacturing.

The increasing demand for rare earth elements (REEs) fuelled by the global shift toward renewable energy and the growth of high-tech industries has raised significant concerns regarding supply chain vulnerabilities.

The concentration of REE mining, processing and refining in a limited number of countries, most notably China has resulted in geopolitical tensions, economic dependencies and strategic manoeuvring among global powers. China’s dominance in REE production and its previous export restrictions have highlighted the potential for these essential materials to serve as geopolitical leverage.

India is actively addressing supply chain vulnerabilities by developing strategic trade corridors, including the India-Middle East-Europe Corridor (IMEC), the Eastern Maritime Corridor, and the North-South Transport Corridor, to enhance the security and efficiency of its trade routes. The initiative was highlighted during the Singapore Maritime Week in March 2025. Additionally, discussions are underway between India and Singapore to establish a green and digital corridor, aimed at integrating sustainable and technology-driven solutions within maritime trade networks.

India’s supply chain and defence manufacturing sector face heightened challenges due to a broader shift in industrial supply chains towards East Asia, particularly China. This transition has rendered India’s supply chain increasingly vulnerable, especially during times of conflict. China’s dominance in the global supply chain is reinforced by its substantial research and development (R&D) investments, extensive civilian industrial base, and leadership in high-tech manufacturing. [1]

Additionally concerns regarding the ownership structures of firms some of which are based in allied nations but possess significant Chinese investment further complicate India’s strategic supply chain security.

Taiwan and Israel, as global leaders in electronics and semiconductor industries, play a crucial role in defence manufacturing. However, the over-concentration of critical components and materials in a limited number of suppliers poses significant risks, necessitating a strategic push towards diversification to enhance supply chain resilience.

This research aims to analyse the geopolitical significance of REEs, assess the risks associated with global supply chains, and evaluate the environmental challenges posed by their extraction and processing. The study examines how nations are responding to REE dependencies, the strategies being implemented to diversify supply chains, and their broader implications for international relations, economic security and technological advancements.

Objectives of the Research –

Literature Review –

In his paper, “The Geopolitics of Rare Earth Elements: Emerging Challenge for U.S. National Security and Economics”, Bert Chapman explores the strategic importance of rare earth elements (REEs) in the U.S., focusing on their economic, technological and national security implications.

The paper outlines the critical role RREs play in modern technologies, such as modern military weapons and electronics powered by renewable energy. The author discusses U.S. dependency on foreign RRE supplies, particularly China, which controls the majority of global production and emphasises the risks this dependency poses to national security and economic stability.

In his paper, New Energy Geopolitics Shaped by Energy Transition: The Energy Balance for Rare Earth Elements and Critical Minerals", Cemal Kakisim examines the shifting geopolitics surrounding rare earth elements and critical minerals driven by the global energy transition.

The study highlights how the global shift from fossil fuels to renewable energy sources like wind, solar, and geothermal has created new dependencies on RREs and critical minerals such as lithium, cobalt, and neodymium.

In her Geopolitical Power Through Critical Mineral Resources thesis, Isabella Huang investigates the evolving dynamics of geopolitical influence tied to rare earth elements (REEs) and critical minerals.

The study emphasises the indispensability of REEs in high-technology applications, military systems, and green energy transitions; it explores how REEs have become a vital tool for geopolitical leverage in the global arena.

The article entitled “Rare Earths and Geopolitics: An Increasingly Messy Mix (2023) by Tobias Burgers and Scott N. Romaniuk explores the Strategic importance of REMs (Rare Earth Metals) and their implications for international relations, especially in the context of China’s dominance in their supply chain.

A key argument presented in the article is that China’s control over REM has fuelled anxieties among its geopolitical rivals, particularly the U.S. and its allies. The possibility of China using REM exports as a bargaining chip in diplomatic conflicts has led to discussions about supply chain diversification. In 2023, China imposed new export restrictions on certain REMs, reinforcing the perception that Beijing could exploit its dominance for strategic purposes.

Energy Transition: Renewable Energy Sources and Emerging Energy Technologies

The transition from fossil fuels to renewable energy sources marks a significant transformation in the global energy landscape. Historically, energy transitions have been driven by technological advancements and environmental considerations, progressing from wood and waterpower to coal, then to oil and natural gas, and recently towards renewable sources such as solar, wind, geothermal and biomass energy (Gielen et al., 2019).

The increasing global reliance on these cleaner energy alternatives directly responds to mounting concerns over climate change, energy security and sustainability of fossil fuel consumption.

International environmental agreements, such as the Paris Agreement of 2016, have catalysed the widespread adoption of renewable energy. Many nations have responded by prioritising investments in renewable energy infrastructure and technological advancements in energy storage, electric mobility, and smart grids.

Consequently, the share of renewables in global energy consumption has increased significantly, rising from 6.6% in 1990 to approximately 12.2% by 2019 (British Petroleum, 2020). Projections from the International Energy Agency (IEA) suggest renewables could account for nearly 63% of global primary energy consumption by 2050 (IEA,2021).

Renewable energy production, however, requires a fundamentally different set of raw materials than fossil-fuel-based systems. The infrastructure supporting solar panels, wind turbines and energy storage technologies depends on critical minerals such as lithium, cobalt, germanium and tellurium. These materials, collectively known as REEs, are essential in the global energy transition. For instance, lithium-ion batteries integral to both renewable energy storage and electric vehicles – have driven an unprecedented demand for lithium and cobalt, with projections estimating a tenfold increase in demand for lithium by 2030 (Swain, 2017).

Rivalia Chemical, a startup founded in 2021 by environmental engineer Laura Stoy, is developing a technology to address the environmental and health hazards of ash ponds by repurposing coal ash as a domestic source of rare earth elements. Stoy’s flagship extraction technology is supported by the Georgia Institute of Technology.[2]

The company’s technology employs a multi-step process to extract REEs from coal ash, leaving behind a solution rich in these elements and a residual solid containing iron and other metals. The extraction process relies on a proton exchange mechanism, in which REEs are transferred into an ionic liquid a salt in a liquid state through sequential heating and cooling steps. Acid-base reduction techniques and salt-based leaching help minimize the presence of iron in the final solution, after which REEs must be further separated to yield pure metals or oxides.

Global Importance of REEs –

The United States has reopened and invested in its domestic sources of REEs, such as the Mountain Pass mine in California. Additionally, the US has partnered with countries like Australia and Canada to explore new mining opportunities and establish reliable supply chains. Similarly, the European Raw Materials Alliance has been formed within the European Union to enhance the extraction and refinement of rare earth metals.

It is also important to recognise that international alliances are increasingly significant in the geopolitics surrounding rare earth elements. Through collaboration, it is possible to diversify supply chains and reduce the REE market’s vulnerability to China's monopolistic influence.

A notable example is the Quad Alliance (U.S., Japan, India, and Australia), which has discussed cooperation to secure critical supply chains for minerals, including rare earth elements. The formation of alliances in the realm of rare earth elements transcends mere geographic considerations, incorporating critical economic, environmental and technological dimensions. Collaborative efforts among nations facilitate the establishment of robust and diversified supply chain networks that mitigate dependence on singular sources.

The U.S. Department of Defence has allocated over 439$ million in funding since 2020 to foster a new domestic supply chain, encompassing the separation and refining of materials mined within the U.S. as well as downstream production of magnets. In line with broader trends to friend-shoring critical mineral supplies, The DoD recognizes Canada, Australia and the UK as domestic partners. Several Western countries reported advancements in their efforts to enhance production capacity. Northeast Wyoming, is home to some of the highest-grade deposits in North America and is a key focus for firms such as Wyoming Rare USA and Rare Earth Elements Resources, which are seeking to develop these resources.

Additionally, projects across the U.S. include Re Elements Technologies in Indiana, Rainbow Rare Earth in Florida and Lynas in Texas. Meanwhile, Energy fuels in Utah and Phoenix Tailings in Massachusetts are already in production and are scaling up their output to meet market demand. These facilities aim to diversify the supply chain throughout the United States, building on the foundation of MP materials in California, which has previously been the sole commercial-scale operation in the country.

Given these dynamics, Pakistan has also emerged as a key strategic player in the REEs due to its geographic position and prospective abundance of Rare Earth elements. The northern regions of the country, encompassing the Karakorum terrain and Kohistan Island arc, are known to host significant REE resources.

Extensive exploration has identified eight zones within the Khyber Pakhtunkhwa province, extending approximately 200 kilometres from Mansehra to the Pakistan-Afghanistan border, with the potential to harbour substantial REE deposits. Pakistan’s inability to effectively leverage its resources has resulted in a lag in an industry that is pivotal to shaping the geopolitical and economic future of nations. If Pakistan can address its technological and infrastructural challenges, it has the potential, not only to transform its economic trajectory but also forge strategic partnerships that enhance trade relations with global players. However, failing to act decisively may result in lost opportunities, leaving the nation reliant on traditional exports while others benefit from its untapped resources.

Japanese researchers have discovered significant deposits of rare earth metals, including cobalt and nickel, in the seabed off Minami-Torishima Island. Studies from Tokyo University estimate that these amounts could be sufficient to meet Japan’s consumption needs for decades, potentially reducing the country’s reliance on imports.

There have been plans by the Japanese government to initiate a trial collection of manganese nodules, or mineral concretions, from the Pacific Ocean site in early 2025, with an eye towards commercialization. A research team surveyed from April to June to identify mineral resources scattered across the seabed at depths ranging from 5,200 to 5,700 meters off the island, which is part of the Ogasawara Island chain.

According to a comprehensive survey covering 10,00 square kilometres, researchers estimate that approximately 230 million tons of manganese nodules exist in the area. These nodules are believed to contain around 610,000 tons of cobalt which is equivalent to 75 years of Japan’s domestic consumption and approximately 740,000 tons of nickel, enough to meet Japan’s need for 11 years. The operation is anticipated to commence in 2025, during which researchers aim to extract about 2,500 tons of manganese nodules daily, targeting a total of 3 million tons annually.

Cobalt nickel, and other rare metals are critical components in electric vehicles, smartphones and various advanced electronic products. However, Japan relies on imports for these materials as they are primarily concentrated in regions like Africa and Australia. The availability of REE resources in Africa is substantial, warranting further exploration and development. An estimated four million tonnes of contained rare earth oxides are present across various projects.

Extensive geological formations with REE-bearing potential remain largely unexplored. For instance, numerous carbonatite formations along the East African Rift Valley hold significant promise for additional Ree discoveries. Preliminary analysis samples from carbonatites and associated fenites. In Uganda’s eastern Rift Valley hold has consistently exhibited economic grade REE concentrations, justifying further investigation. However, the primary challenge lies in the strategic intent to enter the REE market, necessitating a comprehensive market and value chain analysis.

China’s dominance in REEs –

China has maintained a near monopoly on the global supply of rare earth metals, commanding approximately 85% to 95% of the market since the late 1990s. This substantial control over the REE supply chain has raised alarms regarding the potential for geopolitical manoeuvres in response to international tensions. Notably, in 2010, during escalating territorial disputes with Japan over the Senkaku/Diaoyu Islands, China explicitly indicated the possibility of restricting their exports to Japan, underscoring the strategic importance of these materials in global politics.

Before the rise of China’s influence, the United States held a dominant position in the production and distribution of rare earth elements. However, this supremacy was surrendered to China, likely due to legal constraints regarding radioactive materials. Following the exodus of the industry from the West in the 1980s, China dedicated the subsequent decades towards exploring and developing its interior regions, ultimately establishing the world’s largest REE mine in its northern territory.

According to Klinger (2017), China’s pursuit of REE development was driven not only by economic considerations but also by political factors, both domestic and international. The nation’s monopoly on REEs stemmed from its objectives related to nation-building, territorial disputes with the former Soviet Union and its nuclear ambitions. China’s dominance in the REE market was bolstered by its low labour costs and low environmental standards, which allowed REE exports to be priced so low that competition outside China became economically unfeasible.

Over the past decades, China has established a dominant position in the global supply chain of rare earth elements (Strafor 2020). The absence of a standardised global exchange for REE trading has led some political analysts to view China’s near monopoly as a potential destabilising force in regional geopolitics.

Conversely, others contend that China’s 2011 export restrictions on REEs were primarily driven by domestic considerations, including resource conservation, environmental protection and strategic development of high-tech industries (Biedermann 2014; Wübbeke 2013).

Given the inherent challenges in scaling up the supply of REEs, particularly mined environmental regulations hinder resources and refined metals cost-effective increases. This complexity renders the factors influencing REE import/export dynamics critical to the broad spectrum of global industries.

China’s global dominance in rare earth elements (REEs) is evident in both upstream production and downstream industries, including REE intermediary products (Mancheri 2015). The twelfth five-year plan, announced in May 2011, aimed to enhance energy efficiency, reduce carbon emissions, and position China as the leading global producer of renewable energy.

Magnets, phosphors, hydrogen storage materials, and abrasive polishing materials were among the sectors prioritised for expanding downstream REE industries and promoting advanced manufacturing. Consequently, the government consolidated the REE industry, merging over 100 firms into six state-owned enterprises and directly funding national research laboratories focused on REE smelting and separation.

These SOEs were responsible for 99.9% of China’s REE production quota in the first half of 2016. Following the merger of three major mining conglomerates and two research institutes in 2022 to form the China Rare Earth Group, China is now projected to control 30 to 40% of the global supply. Under the direct supervision of the State Council, the newly established SOE is expected to strengthen China’s ability to dictate prices for key REEs, potentially disrupting the supply chain (Zhou and Brooke, 2022).

Vekasi (2022) suggests that further consolidation within the REE industry will be driven by objectives such as enhancing state control, addressing domestic supply and demand disparities, promoting vertical integration and ensuring price stability. An analysis of trading data for rare earth elements indicates that the prices of the metals imported by Japan are positively correlated with the exporting country’s level of geopolitical risk. This suggests that rising geopolitical tensions between exporting nations and other countries can increase the prices of rare earth elements.

Additionally, the analysis shows that the gross value of imported rare earth elements is negatively correlated with geopolitical risk, with this relationship being particularly pronounced when rare earth elements are sourced from China. The data suggests that when accounting for uncertainties in Japan’s economic policies, the statistical significance between rare earth elements and geopolitical risk diminishes, except for geopolitical risks associated with China. These findings highlight the extent to which the volume of REE exports in China is inherently shaped by geopolitical considerations.

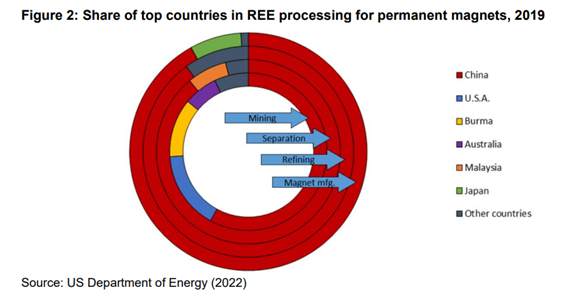

Furthermore, Japan’s REE imports used to have a negative connection with geopolitical risks in China. However, during the World Trade Organization (WTO) dispute about China’s REE export limits, this connection weakened. This change might be due to a rise in illegal REE exports and a drop in export quotas, these Shifts were likely affected by political developments in China during the time. China currently holds a dominant position in manufacturing permanent magnets, producing both high-performance sintered NdFeB magnets and bonded NdFeB magnets (NdFeB permanent magnet has a stronger magnetic field than alternatives, reducing the weight and dimensions of large turbines, no external power system is needed, resulting in greater efficiency and simpler design). This technology was developed in 1983 through a collaboration between General Motors and Sumitomo Corp.

While both companies initially manufactured permanent magnets in the U.S. for several years, high production costs and closures of the Mountain Pass mine led to a shift in production to Asia, first to Japan and then subsequently to China. Most of the primary intellectual property related to NdFeB magnets has expired; however, firms in the U.S. and Japan continue to advance their intellectual property in this field.

Despite China accounting for approximately 90% of global NdFeB capacity, Germany and Japan maintain a portion of the market, with Japanese firms also operating manufacturing facilities in Malaysia and Thailand.

Following the classification of NdFeB batteries as a critical national security technology in 2021, U.S. policies anticipated to enhance the manufacturing of the magnets, aiming for an estimated 50% self-sufficiency in sintered NdFeB production by 2030.

Despite a decline in China’s market share within the upstream mining sector, its absolute supply output continues to rise. Importantly, its dominance across the intricate midstream to downstream processing and manufacturing stages proves increasingly difficult to challenge. Although rare earths are relatively abundant geologically, they are considered rare due to the complexities involved in extracting and separating the ores into individual oxides necessary for manufacturing. This difficulty makes economically viable deposits scarce.

The consolidated, state-controlled Chinese market remains at the forefront of industrial and technologically demanding operations related to rare earth processing. In December 2023, China implemented export controls on technologies essential for rare earth extraction, separation, refining and magnet production, potentially impending new developments outside its borders. China’s dominance in the rare earth elements industry is an exemplification of decades of strategic investment and market control but also highlights vulnerabilities in global supply chains and evident reliance on a single player. Rare earths are indispensable to modern technology and defence, and their demand is only set to increase as industries expand and transition to cleaner solutions.

On December 3 2024, China’s Ministry of Commerce announced that it would stop exporting gallium, germanium, antimony and superhard materials to the United States. This decision was made due to the dual nature of these materials, which can serve both military and civilian applications.

The ministry also indicated that there will be more stringent checks on the export of graphite. These rare materials are crucial to produce semiconductors, electronics, weapons, solar energy technologies, electric vehicles and more. The bans extend to restrict trans-shipment through third-party nations, forcing global companies to choose between the U.S. and China. This shift is likely to precipitate disruptions and shortages that may extend to other essential minerals such as nickel and cobalt which are critical for various industrial applications.

The U.S. defence sector heavily depends on rare earth elements, making supply chain disruptions a critical risk to maintaining strategic parity with China’s advancing military capabilities. Reports indicate that China is currently outpacing the U.S. in the development of advanced weaponry and munitions. A recent U.S. Geological Survey estimated that a complete export ban on gallium and germanium could result in an economic loss of approximately 3.4$ billion in U.S. GDP. Additionally, while graphite exports have not been fully restricted, increasingly stringent regulations pose another significant risk. The U.S. holds less than 1% of the world’s graphite reserves and is therefore entirely dependent on imports.

In contrast, China possesses the highest of the world’s graphite reserves and dominates global production, accounting for 78% of natural graphite over 95% of synthetic graphite, and nearly 100% of graphite refining.

The significance of these figures is particularly relevant to the EV industry, as EV requires approximately 136 pounds of graphite. The Inflation Reduction Act is projected to generate 99,600 within the EV sector, highlighting the potential economic ramifications should China impose a full graphite export ban.

Beyond minerals, China has also taken steps to undermine the reputation of the U.S. semiconductor industry. The announcement of rare mineral export restrictions coincided with the China Semiconductor Industry Association cautioning domestic firms against purchasing American chips.

The association warned that “American chip products are no longer safe and reliable, and related Chinese industries will have to be cautious in purchasing American chips”. Such statements could lead to financial losses for U.S. semiconductor manufacturers by reducing their market share in China and further straining economic relations between the two nations.

China’s Export Controls and India’s Response –

China’s imposition of export restrictions on rare earth’s export is a direct response to escalating geopolitical tensions and trade restrictions by Western nations, particularly the U.S. Measures such as export controls on advanced technologies and restrictions on foreign investments have contributed to an environment of heightened strategic competition and mutual distrust. From China’s perspective, these policies are perceived as deliberate efforts to curtail its technological and economic advancement. China’s export restrictions can therefore be understood as both a retaliatory measure and a strategic counter-move. As an act of retaliation, these restrictions serve as a direct response to trade and investment limitations imposed by Western nations.

Simultaneously, as a countermeasure, China is leveraging its dominant position in the global rare earth supply chain to mitigate the economic and technological impact of the Western sanctions. REEs are subject to price volatility, and China’s export restrictions have the potential to further destabilize the market. A reduction in the availability of these critical materials could drive up costs for manufacturers, ultimately leading to higher retail prices for consumer goods that rely on rare earth, including smartphones, electric vehicles and renewable energy technologies.

For many industries, the rising costs of essential raw materials would erode the profit margins or necessitate price increases, thereby affecting end consumers. In response to China’s restrictions on critical materials, India must adopt a multifaceted strategy to enhance the resilience of its supply chains. Strengthening domestic manufacturing is a key priority, as boosting local capabilities can significantly reduce the dependency on imports. Government initiatives such as Make in India should be leveraged to foster a robust manufacturing ecosystem, enabling the country to develop self-sufficiency in key industries.

Additionally, diversifying trade partnerships is essential for securing alternative sources of critical materials.

Collaborating with technologically advanced nations such as Japan and South Korea can provide India access to high-quality components while reducing vulnerabilities associated with overreliance on a single supplier. These alliances can facilitate knowledge transfer, improve supply chain stability, and enhance India’s integration into global value chains.

Prime Minister Modi in his recent diplomatic visit to the U.S. engaged in bilateral discussions with President Donald Trump on a broad range of strategic issues, including trade, technology, defence, security, energy etc. A key outcome of the visit was the launch of the India-U.S. TRUST (Transforming the Relationship Utilizing Strategic Technology) initiative, which aims to enhance bilateral cooperation in critical and emerging technologies.

Under these initiatives, both leaders committed to strengthening trusted and resilient supply chains, particularly in semiconductors, critical materials, advanced materials and pharmaceuticals. Recognizing the strategic significance of critical materials for emerging technologies and advanced manufacturing, the United States and India agreed to accelerate collaboration in research and development while promoting investment across the entire critical mineral value chain. Both nations pledged to deepen engagement through the Mineral Security Partnership, an international framework aimed at ensuring the securing and sustainable supply of critical minerals.

Investing in R&D is another crucial element of India’s strategy. Advancing Indigenous technologies in areas such as solar panels, semiconductors, and electric vehicle (EV) batteries can reduce dependency on foreign suppliers and enhance India’s technological capabilities. By fostering innovation and promoting domestic R&D efforts, India can position itself as a competitive player in emerging industries while mitigating the risks associated with global supply chain disruptions.

Environment Challenges Related to Rare Earth Elements –

The types of REE deposits can significantly impact environmental outcomes as their processing methods differ based on the physicochemical properties of the deposits (Weng 2013). Key concerns typically include the substantial use of chemicals (such as acids and alkalis), the concentration of REEs in tailings and the presence of radioactive elements (Thorium and Uranium) in the ores. REE deposits primarily occur in four geological environments (Weng 2013; Dostal 2017): carbonatites, alkaline igneous systems, ion–ion-absorption clay deposits (predominantly in China), and monazite-bearing placer deposits.

The primary REE-containing mineral types are carbonite and alkaline igneous deposits; hence, the generation of mine tailings and the potential release of radionuclides pose significant environmental risks for REE development. REEs are mined by digging vast open pits in the ground, which can contaminate the environment and disrupt ecosystems. If poorly regulated, mining can produce wastewater ponds filled with acids, heavy metals, and radioactive material that might leak into groundwater.

The Bayan Obo stands out as the largest rare earth element mine globally, but its significance is often eclipsed by the environmental challenges posed by its tailings pond. The facility has accumulated over 70,000 tons of radioactive thorium, raising serious concerns due to the absence of adequate liners.

As a result, radioactive leachates are infiltrating the surrounding groundwater, with projections indicating that these contaminants may eventually end up in Yellow River, an essential source of potable water.

The Harvard International Review reported that the extraction of one ton of rare earth elements generates approximately 30 pounds of dust, between 9,600 and 12,000 cubic meters of waste gas – including hazardous substances like hydrofluoric acid and sulphur dioxide - 75 cubic meters of wastewater and one ton of radioactive residue. In total, this process results in around 2,000 tons of toxic waste.[1]

An effective strategy to mitigate the reliance on rare earth elements in manufacturing is for engineers and designers to create products that either minimise the usage of these elements or substitute them with alternative materials. Automotive manufacturers such as BMW and Renault have developed electric vehicles devoid of rare earth elements.

Recently, Tesla announced that its forthcoming generation of electric motors will eliminate the use of rare earth elements (REEs). Additionally, since 2017, Tesla has achieved a 25% reduction in heavy REEs in its Model 3 production. Tesla has acknowledged concerns regarding the supply chain stability and environmental impact of rare earth mineral extraction, particularly in the context of its electric vehicle production.

Colin Campbell, a member of Tesla’s powertrain executive team, presented data to investors indicating that the motors in the Tesla Model Y contain approximately 520 grams of REEs. These minerals primarily used in neodymium-based magnets are essential for generating a magnetic field strong enough to facilitate vehicular motion. In response to these challenges, Tesla introduced a next-generation permanent magnet motor that eliminates the need for rare earth elements. The company has not disclosed specific elements being removed, neodymium is believed to be the primary target, given its significant presence in Motor Y.

Researchers and industry experts have identified several potential alternatives to REEs for EVs. According to William Roberts, a senior research analyst at London-based consultancy Rho Motion, ferrite magnets composed of iron and combined with elements such as barium and strontium offer a more widely available and cost-effective alternative to rare earth-based magnets.

General Motors (GM) has previously incorporated ferrite magnets into its motor designs and in December 2023, Japan-based Proterial Ltd announced the development of motors using Ferrite magnets that matched the performance of components traditionally dependent on rare earth elements. As the demand for REE grows, there is a growing pressure to expand domestic production, which may come at the cost of environmental considerations. Governments should focus on drafting policies establishing geopolitically stable supply chains, enforcing sustainable mining and refining practices, and promoting flexibility and innovation in the use of REEs.

Emerging Players and Partnerships in REE –

As China’s dominant rare earth element (REE) reserves face depletion and emergent REE mining opportunities arise in Africa and South America, Beijing has intensified its exploratory initiatives, identifying prospective extraction sites across Southeast Asia. Presently, Malaysia, Thailand, and Vietnam occupy notable positions within the global REE supply chain.

The strategic viability of these nations as alternative suppliers is contingent upon a constellation of factors, including the magnitude and mineralogical composition of their REE deposits, their technical and infrastructural mining capabilities, and their engagement across various stages of the value chain – namely, upstream extraction, midstream processing and downstream manufacturing and end-use applications. Their ability to serve as reliable alternatives will significantly Their ability to serve as reliable alternatives will significantly depend on the coherence and competitiveness of these integrated operations.

On the production front, Vietnam mines about 600 tonnes of REE per year, but has 22 million tonnes of REE reserves- half the size of China’s reserves. Malaysia mined 80 tonnes of REE since 2024; its government has not disclosed official estimates of REE reserves but claims to have 16 million tonnes of non-radioactive REEs. These numbers suggest that while Southeast Asian countries such as Vietnam and Malaysia may have substantial reserves, their current REE production levels are significantly lower than China’s. [2]

Vietnam South Korea US Joint Venture: South Korea’s Trident Global Holdings and the US’s Zoetic Global have formed a joint venture with Vietnam’s Hung Hai Group to develop and process rare earth mines in northern Vietnam. This partnership aims to leverage eco-friendly technologies and secure a sustainable supply of REEs, particularly for US technology, aerospace and defence sectors.

Australia is seen as a natural partner for Vietnam to unlock the potential of its REE reserves. While no Australian REE companies currently operate in Vietnam, companies like Blackstone Minerals are leading by example with sustainable mining projects such as the Ta Khoa nickel-copper project. This project aims to meet high ESG (Environmental, Social and Governance) standards, showcasing the viability of responsible resource development in Vietnam.

The partnership is mutually beneficial –

Latin America holds some 60% of the world’s lithium reserves and another 40% of copper reserves, as per IEA data, and is home to seven of the world’s 10 most productive copper mines. Moreover, most of the world’s top-producing countries for the two metals are in the region, with Bolivia, Argentina, and Chile spearheading the list for lithium and Chile and Peru for copper. [3]

Brazil, the region’s largest economy and home to the world’s third-largest reserves of nickel and rare earth elements has allocated $815 million to support projects focused on sustainable and technological development, as stated by Aloizio Mercadante, the president of Brazil’s National Development Bank.

In Chile, the government-operated copper ming company Codelco had entered into a 35-year agreement with lithium manufacturer Sociedad Quimica y Minera de Chile to co-develop extensive lithium resources in the Salar de Atacama salt flat from 2025 to 2060, intending to enhance domestic control over mainstream lithium sector.

In Argentina, a notable advancement has emerged from the government, which recently signed a cooperation agreement with the United States aimed at diversifying the latter’s long-term sourcing away from China.

Emerging Alliances and New Extraction Technologies in Rare Earth Elements –

Researchers at the University of Texas at Austin have developed an innovative technique that enables the separation and extraction of REEs in geopolitical contexts where conventional methods are currently unfeasible. This advancement is particularly salient in light of increasing geopolitical tensions affecting global trade in strategic minerals. The method employs synthetic membrane channels – nanoscale pores incorporated into membranes – that emulate ion-selective transport mechanisms observed in biological systems, specifically those mediated by transmembrane proteins.

The scientists designed the channels using a special chemical structure called pillar arene, which they modified to attract and carry specific REEs while blocking other common ions like potassium, sodium and calcium. The result is a system that can target and move specific rare earth elements, such as europium and terbium, making the process more precise and efficient.

QUAD holds potential to become the mitigation to India’s REE challenge. In Oct 2024, India announced a major agreement – critical minerals supply chain cooperation with the US. The two sides committed to “expand and diversify” supply chains and benefit from each other’s strengths. This highlights India as a potential key partner in the efforts worldwide led by the US to diversify away from China’s dominance and India’s quest for technology transfers.

The India-US collaboration on Critical and Emerging Technology (iCET) is an attempt in this direction in which both countries are exploring critical mineral diversification efforts. Australia, not only holds large REE reserves, but also a technical edge over India in large-scale production. India and Australia already have bilateral cooperation on critical minerals which can be extended to rare earths. Furthermore, India can partner with the Japan Organization for Metals and Energy Security (JOGMEC) for sharing high-end technology and experience in the field of REEs. India is already part of the 15-member group known as the Minerals Security Partnership, an informal association of nations to manage divergence efforts for mineral dependency. Finally, the government has to prioritize its efforts, promote private industry and invest in R&D for niche technology to achieve self-reliance.[4]

Saudi Arabia has emerged as a potential game-changer in the future of the rare earth supply chain. Its strategic geographical position between Eastern and Western markets provides natural advantages for becoming a processing hub serving multiple markets. The Kingdom offers competitive advantages including low-cost energy and feedstock—critical factors in rare earth processing economics. With some of the world's lowest electricity costs and abundant natural gas for chemical processes, Saudi Arabia could potentially process rare earth concentrates at costs approaching Chinese levels.

Recent exploration has revealed that Saudi Arabia possesses abundant rare earth resources, particularly in the Arabian Shield region. According to geological surveys, some deposits show concentrations comparable to major producing regions globally.[5]

Conclusion –

The strategic importance of REEs in shaping global geopolitics, technological advancements and energy transition cannot be overstated. These critical materials form the foundation of modern innovation from renewable energy to advanced military systems making them indispensable to the global economy. However, the concentration of REE production in China has created significant vulnerabilities, exposing other nations to supply chain disruptions, geopolitical tensions and trade uncertainties.

To mitigate the risks, nations must adopt a multi-faceted approach to reducing their reliance on China while ensuring long-term sustainability in REE supply chains. Policy initiatives should strengthen domestic mining and processing collaborations and invest in technological innovations. Countries such as the U.S. Japan and the European Union have already initiated cooperative agreements to diversify supply chains and reduce dependency on a single source.

REEs have emerged as focal points in geopolitical competition due to their essential role in defence systems, renewable energy and advanced technologies. China’s dominance in extraction accounting for 58% of global mining and processing representing 85% to 85% of the global supply provides the country with significant strategic leverage, as evidenced by past trade disputes and export restrictions.

To address these vulnerabilities, nations are implementing diversified strategies with an emphasis on supply chain resilience, technological innovation and international collaboration. Countries are forging partnerships with resource-rich nations such as Australia, the world’s non-Chinese REE producer as well as Vietnam and Brazil to secure vital raw materials.

In light of the strategic significance of REEs in underpinning modern technologies and their critical role in global power dynamics, states must adopt a comprehensive approach to securing their REE supply chains. This necessitates sustained investment in research and development to drive innovation in extraction, processing and recycling technologies, thereby reducing environmental impact and increasing efficiency.

It is imperative to develop a favourable regulatory framework for domestic REE ming and processing in order to reduce external dependencies. Establishing strategic reserves can serve as a vital buffer against market disruptions and geopolitical shocks. Lastly, mobilizing private sector engagement will be crucial to scaling infrastructure and ensuring long-term resilience.

Bibliography –

Rare Earth Elements (REEs) comprise 17 critical minerals essential for various advanced technologies, including renewable energy systems, defence applications and consumer electronics. Their unique chemical and physical properties make them indispensable in modern industries, from electric vehicles and wind turbines to missile guidance systems and semiconductor manufacturing.

The increasing demand for rare earth elements (REEs) fuelled by the global shift toward renewable energy and the growth of high-tech industries has raised significant concerns regarding supply chain vulnerabilities.

The concentration of REE mining, processing and refining in a limited number of countries, most notably China has resulted in geopolitical tensions, economic dependencies and strategic manoeuvring among global powers. China’s dominance in REE production and its previous export restrictions have highlighted the potential for these essential materials to serve as geopolitical leverage.

India is actively addressing supply chain vulnerabilities by developing strategic trade corridors, including the India-Middle East-Europe Corridor (IMEC), the Eastern Maritime Corridor, and the North-South Transport Corridor, to enhance the security and efficiency of its trade routes. The initiative was highlighted during the Singapore Maritime Week in March 2025. Additionally, discussions are underway between India and Singapore to establish a green and digital corridor, aimed at integrating sustainable and technology-driven solutions within maritime trade networks.

India’s supply chain and defence manufacturing sector face heightened challenges due to a broader shift in industrial supply chains towards East Asia, particularly China. This transition has rendered India’s supply chain increasingly vulnerable, especially during times of conflict. China’s dominance in the global supply chain is reinforced by its substantial research and development (R&D) investments, extensive civilian industrial base, and leadership in high-tech manufacturing. [1]

Additionally concerns regarding the ownership structures of firms some of which are based in allied nations but possess significant Chinese investment further complicate India’s strategic supply chain security.

Taiwan and Israel, as global leaders in electronics and semiconductor industries, play a crucial role in defence manufacturing. However, the over-concentration of critical components and materials in a limited number of suppliers poses significant risks, necessitating a strategic push towards diversification to enhance supply chain resilience.

This research aims to analyse the geopolitical significance of REEs, assess the risks associated with global supply chains, and evaluate the environmental challenges posed by their extraction and processing. The study examines how nations are responding to REE dependencies, the strategies being implemented to diversify supply chains, and their broader implications for international relations, economic security and technological advancements.

Objectives of the Research –

- To assess the geopolitical importance of the REEs

- To Analyze China’s dominance in the global REE supply chain

- To Evaluate the environmental challenges

Literature Review –

In his paper, “The Geopolitics of Rare Earth Elements: Emerging Challenge for U.S. National Security and Economics”, Bert Chapman explores the strategic importance of rare earth elements (REEs) in the U.S., focusing on their economic, technological and national security implications.

The paper outlines the critical role RREs play in modern technologies, such as modern military weapons and electronics powered by renewable energy. The author discusses U.S. dependency on foreign RRE supplies, particularly China, which controls the majority of global production and emphasises the risks this dependency poses to national security and economic stability.

In his paper, New Energy Geopolitics Shaped by Energy Transition: The Energy Balance for Rare Earth Elements and Critical Minerals", Cemal Kakisim examines the shifting geopolitics surrounding rare earth elements and critical minerals driven by the global energy transition.

The study highlights how the global shift from fossil fuels to renewable energy sources like wind, solar, and geothermal has created new dependencies on RREs and critical minerals such as lithium, cobalt, and neodymium.

In her Geopolitical Power Through Critical Mineral Resources thesis, Isabella Huang investigates the evolving dynamics of geopolitical influence tied to rare earth elements (REEs) and critical minerals.

The study emphasises the indispensability of REEs in high-technology applications, military systems, and green energy transitions; it explores how REEs have become a vital tool for geopolitical leverage in the global arena.

The article entitled “Rare Earths and Geopolitics: An Increasingly Messy Mix (2023) by Tobias Burgers and Scott N. Romaniuk explores the Strategic importance of REMs (Rare Earth Metals) and their implications for international relations, especially in the context of China’s dominance in their supply chain.

A key argument presented in the article is that China’s control over REM has fuelled anxieties among its geopolitical rivals, particularly the U.S. and its allies. The possibility of China using REM exports as a bargaining chip in diplomatic conflicts has led to discussions about supply chain diversification. In 2023, China imposed new export restrictions on certain REMs, reinforcing the perception that Beijing could exploit its dominance for strategic purposes.

Energy Transition: Renewable Energy Sources and Emerging Energy Technologies

The transition from fossil fuels to renewable energy sources marks a significant transformation in the global energy landscape. Historically, energy transitions have been driven by technological advancements and environmental considerations, progressing from wood and waterpower to coal, then to oil and natural gas, and recently towards renewable sources such as solar, wind, geothermal and biomass energy (Gielen et al., 2019).

The increasing global reliance on these cleaner energy alternatives directly responds to mounting concerns over climate change, energy security and sustainability of fossil fuel consumption.

International environmental agreements, such as the Paris Agreement of 2016, have catalysed the widespread adoption of renewable energy. Many nations have responded by prioritising investments in renewable energy infrastructure and technological advancements in energy storage, electric mobility, and smart grids.

Consequently, the share of renewables in global energy consumption has increased significantly, rising from 6.6% in 1990 to approximately 12.2% by 2019 (British Petroleum, 2020). Projections from the International Energy Agency (IEA) suggest renewables could account for nearly 63% of global primary energy consumption by 2050 (IEA,2021).

Renewable energy production, however, requires a fundamentally different set of raw materials than fossil-fuel-based systems. The infrastructure supporting solar panels, wind turbines and energy storage technologies depends on critical minerals such as lithium, cobalt, germanium and tellurium. These materials, collectively known as REEs, are essential in the global energy transition. For instance, lithium-ion batteries integral to both renewable energy storage and electric vehicles – have driven an unprecedented demand for lithium and cobalt, with projections estimating a tenfold increase in demand for lithium by 2030 (Swain, 2017).

Rivalia Chemical, a startup founded in 2021 by environmental engineer Laura Stoy, is developing a technology to address the environmental and health hazards of ash ponds by repurposing coal ash as a domestic source of rare earth elements. Stoy’s flagship extraction technology is supported by the Georgia Institute of Technology.[2]

The company’s technology employs a multi-step process to extract REEs from coal ash, leaving behind a solution rich in these elements and a residual solid containing iron and other metals. The extraction process relies on a proton exchange mechanism, in which REEs are transferred into an ionic liquid a salt in a liquid state through sequential heating and cooling steps. Acid-base reduction techniques and salt-based leaching help minimize the presence of iron in the final solution, after which REEs must be further separated to yield pure metals or oxides.

Global Importance of REEs –

The United States has reopened and invested in its domestic sources of REEs, such as the Mountain Pass mine in California. Additionally, the US has partnered with countries like Australia and Canada to explore new mining opportunities and establish reliable supply chains. Similarly, the European Raw Materials Alliance has been formed within the European Union to enhance the extraction and refinement of rare earth metals.

It is also important to recognise that international alliances are increasingly significant in the geopolitics surrounding rare earth elements. Through collaboration, it is possible to diversify supply chains and reduce the REE market’s vulnerability to China's monopolistic influence.

A notable example is the Quad Alliance (U.S., Japan, India, and Australia), which has discussed cooperation to secure critical supply chains for minerals, including rare earth elements. The formation of alliances in the realm of rare earth elements transcends mere geographic considerations, incorporating critical economic, environmental and technological dimensions. Collaborative efforts among nations facilitate the establishment of robust and diversified supply chain networks that mitigate dependence on singular sources.

The U.S. Department of Defence has allocated over 439$ million in funding since 2020 to foster a new domestic supply chain, encompassing the separation and refining of materials mined within the U.S. as well as downstream production of magnets. In line with broader trends to friend-shoring critical mineral supplies, The DoD recognizes Canada, Australia and the UK as domestic partners. Several Western countries reported advancements in their efforts to enhance production capacity. Northeast Wyoming, is home to some of the highest-grade deposits in North America and is a key focus for firms such as Wyoming Rare USA and Rare Earth Elements Resources, which are seeking to develop these resources.

Additionally, projects across the U.S. include Re Elements Technologies in Indiana, Rainbow Rare Earth in Florida and Lynas in Texas. Meanwhile, Energy fuels in Utah and Phoenix Tailings in Massachusetts are already in production and are scaling up their output to meet market demand. These facilities aim to diversify the supply chain throughout the United States, building on the foundation of MP materials in California, which has previously been the sole commercial-scale operation in the country.

Given these dynamics, Pakistan has also emerged as a key strategic player in the REEs due to its geographic position and prospective abundance of Rare Earth elements. The northern regions of the country, encompassing the Karakorum terrain and Kohistan Island arc, are known to host significant REE resources.

Extensive exploration has identified eight zones within the Khyber Pakhtunkhwa province, extending approximately 200 kilometres from Mansehra to the Pakistan-Afghanistan border, with the potential to harbour substantial REE deposits. Pakistan’s inability to effectively leverage its resources has resulted in a lag in an industry that is pivotal to shaping the geopolitical and economic future of nations. If Pakistan can address its technological and infrastructural challenges, it has the potential, not only to transform its economic trajectory but also forge strategic partnerships that enhance trade relations with global players. However, failing to act decisively may result in lost opportunities, leaving the nation reliant on traditional exports while others benefit from its untapped resources.

Japanese researchers have discovered significant deposits of rare earth metals, including cobalt and nickel, in the seabed off Minami-Torishima Island. Studies from Tokyo University estimate that these amounts could be sufficient to meet Japan’s consumption needs for decades, potentially reducing the country’s reliance on imports.

There have been plans by the Japanese government to initiate a trial collection of manganese nodules, or mineral concretions, from the Pacific Ocean site in early 2025, with an eye towards commercialization. A research team surveyed from April to June to identify mineral resources scattered across the seabed at depths ranging from 5,200 to 5,700 meters off the island, which is part of the Ogasawara Island chain.

According to a comprehensive survey covering 10,00 square kilometres, researchers estimate that approximately 230 million tons of manganese nodules exist in the area. These nodules are believed to contain around 610,000 tons of cobalt which is equivalent to 75 years of Japan’s domestic consumption and approximately 740,000 tons of nickel, enough to meet Japan’s need for 11 years. The operation is anticipated to commence in 2025, during which researchers aim to extract about 2,500 tons of manganese nodules daily, targeting a total of 3 million tons annually.

Cobalt nickel, and other rare metals are critical components in electric vehicles, smartphones and various advanced electronic products. However, Japan relies on imports for these materials as they are primarily concentrated in regions like Africa and Australia. The availability of REE resources in Africa is substantial, warranting further exploration and development. An estimated four million tonnes of contained rare earth oxides are present across various projects.

Extensive geological formations with REE-bearing potential remain largely unexplored. For instance, numerous carbonatite formations along the East African Rift Valley hold significant promise for additional Ree discoveries. Preliminary analysis samples from carbonatites and associated fenites. In Uganda’s eastern Rift Valley hold has consistently exhibited economic grade REE concentrations, justifying further investigation. However, the primary challenge lies in the strategic intent to enter the REE market, necessitating a comprehensive market and value chain analysis.

China’s dominance in REEs –

China has maintained a near monopoly on the global supply of rare earth metals, commanding approximately 85% to 95% of the market since the late 1990s. This substantial control over the REE supply chain has raised alarms regarding the potential for geopolitical manoeuvres in response to international tensions. Notably, in 2010, during escalating territorial disputes with Japan over the Senkaku/Diaoyu Islands, China explicitly indicated the possibility of restricting their exports to Japan, underscoring the strategic importance of these materials in global politics.

Before the rise of China’s influence, the United States held a dominant position in the production and distribution of rare earth elements. However, this supremacy was surrendered to China, likely due to legal constraints regarding radioactive materials. Following the exodus of the industry from the West in the 1980s, China dedicated the subsequent decades towards exploring and developing its interior regions, ultimately establishing the world’s largest REE mine in its northern territory.

According to Klinger (2017), China’s pursuit of REE development was driven not only by economic considerations but also by political factors, both domestic and international. The nation’s monopoly on REEs stemmed from its objectives related to nation-building, territorial disputes with the former Soviet Union and its nuclear ambitions. China’s dominance in the REE market was bolstered by its low labour costs and low environmental standards, which allowed REE exports to be priced so low that competition outside China became economically unfeasible.

Over the past decades, China has established a dominant position in the global supply chain of rare earth elements (Strafor 2020). The absence of a standardised global exchange for REE trading has led some political analysts to view China’s near monopoly as a potential destabilising force in regional geopolitics.

Conversely, others contend that China’s 2011 export restrictions on REEs were primarily driven by domestic considerations, including resource conservation, environmental protection and strategic development of high-tech industries (Biedermann 2014; Wübbeke 2013).

Given the inherent challenges in scaling up the supply of REEs, particularly mined environmental regulations hinder resources and refined metals cost-effective increases. This complexity renders the factors influencing REE import/export dynamics critical to the broad spectrum of global industries.

China’s global dominance in rare earth elements (REEs) is evident in both upstream production and downstream industries, including REE intermediary products (Mancheri 2015). The twelfth five-year plan, announced in May 2011, aimed to enhance energy efficiency, reduce carbon emissions, and position China as the leading global producer of renewable energy.

Magnets, phosphors, hydrogen storage materials, and abrasive polishing materials were among the sectors prioritised for expanding downstream REE industries and promoting advanced manufacturing. Consequently, the government consolidated the REE industry, merging over 100 firms into six state-owned enterprises and directly funding national research laboratories focused on REE smelting and separation.

These SOEs were responsible for 99.9% of China’s REE production quota in the first half of 2016. Following the merger of three major mining conglomerates and two research institutes in 2022 to form the China Rare Earth Group, China is now projected to control 30 to 40% of the global supply. Under the direct supervision of the State Council, the newly established SOE is expected to strengthen China’s ability to dictate prices for key REEs, potentially disrupting the supply chain (Zhou and Brooke, 2022).

Vekasi (2022) suggests that further consolidation within the REE industry will be driven by objectives such as enhancing state control, addressing domestic supply and demand disparities, promoting vertical integration and ensuring price stability. An analysis of trading data for rare earth elements indicates that the prices of the metals imported by Japan are positively correlated with the exporting country’s level of geopolitical risk. This suggests that rising geopolitical tensions between exporting nations and other countries can increase the prices of rare earth elements.

Additionally, the analysis shows that the gross value of imported rare earth elements is negatively correlated with geopolitical risk, with this relationship being particularly pronounced when rare earth elements are sourced from China. The data suggests that when accounting for uncertainties in Japan’s economic policies, the statistical significance between rare earth elements and geopolitical risk diminishes, except for geopolitical risks associated with China. These findings highlight the extent to which the volume of REE exports in China is inherently shaped by geopolitical considerations.

Furthermore, Japan’s REE imports used to have a negative connection with geopolitical risks in China. However, during the World Trade Organization (WTO) dispute about China’s REE export limits, this connection weakened. This change might be due to a rise in illegal REE exports and a drop in export quotas, these Shifts were likely affected by political developments in China during the time. China currently holds a dominant position in manufacturing permanent magnets, producing both high-performance sintered NdFeB magnets and bonded NdFeB magnets (NdFeB permanent magnet has a stronger magnetic field than alternatives, reducing the weight and dimensions of large turbines, no external power system is needed, resulting in greater efficiency and simpler design). This technology was developed in 1983 through a collaboration between General Motors and Sumitomo Corp.

While both companies initially manufactured permanent magnets in the U.S. for several years, high production costs and closures of the Mountain Pass mine led to a shift in production to Asia, first to Japan and then subsequently to China. Most of the primary intellectual property related to NdFeB magnets has expired; however, firms in the U.S. and Japan continue to advance their intellectual property in this field.

Despite China accounting for approximately 90% of global NdFeB capacity, Germany and Japan maintain a portion of the market, with Japanese firms also operating manufacturing facilities in Malaysia and Thailand.

Following the classification of NdFeB batteries as a critical national security technology in 2021, U.S. policies anticipated to enhance the manufacturing of the magnets, aiming for an estimated 50% self-sufficiency in sintered NdFeB production by 2030.

Despite a decline in China’s market share within the upstream mining sector, its absolute supply output continues to rise. Importantly, its dominance across the intricate midstream to downstream processing and manufacturing stages proves increasingly difficult to challenge. Although rare earths are relatively abundant geologically, they are considered rare due to the complexities involved in extracting and separating the ores into individual oxides necessary for manufacturing. This difficulty makes economically viable deposits scarce.

The consolidated, state-controlled Chinese market remains at the forefront of industrial and technologically demanding operations related to rare earth processing. In December 2023, China implemented export controls on technologies essential for rare earth extraction, separation, refining and magnet production, potentially impending new developments outside its borders. China’s dominance in the rare earth elements industry is an exemplification of decades of strategic investment and market control but also highlights vulnerabilities in global supply chains and evident reliance on a single player. Rare earths are indispensable to modern technology and defence, and their demand is only set to increase as industries expand and transition to cleaner solutions.

On December 3 2024, China’s Ministry of Commerce announced that it would stop exporting gallium, germanium, antimony and superhard materials to the United States. This decision was made due to the dual nature of these materials, which can serve both military and civilian applications.

The ministry also indicated that there will be more stringent checks on the export of graphite. These rare materials are crucial to produce semiconductors, electronics, weapons, solar energy technologies, electric vehicles and more. The bans extend to restrict trans-shipment through third-party nations, forcing global companies to choose between the U.S. and China. This shift is likely to precipitate disruptions and shortages that may extend to other essential minerals such as nickel and cobalt which are critical for various industrial applications.

The U.S. defence sector heavily depends on rare earth elements, making supply chain disruptions a critical risk to maintaining strategic parity with China’s advancing military capabilities. Reports indicate that China is currently outpacing the U.S. in the development of advanced weaponry and munitions. A recent U.S. Geological Survey estimated that a complete export ban on gallium and germanium could result in an economic loss of approximately 3.4$ billion in U.S. GDP. Additionally, while graphite exports have not been fully restricted, increasingly stringent regulations pose another significant risk. The U.S. holds less than 1% of the world’s graphite reserves and is therefore entirely dependent on imports.

In contrast, China possesses the highest of the world’s graphite reserves and dominates global production, accounting for 78% of natural graphite over 95% of synthetic graphite, and nearly 100% of graphite refining.

The significance of these figures is particularly relevant to the EV industry, as EV requires approximately 136 pounds of graphite. The Inflation Reduction Act is projected to generate 99,600 within the EV sector, highlighting the potential economic ramifications should China impose a full graphite export ban.

Beyond minerals, China has also taken steps to undermine the reputation of the U.S. semiconductor industry. The announcement of rare mineral export restrictions coincided with the China Semiconductor Industry Association cautioning domestic firms against purchasing American chips.

The association warned that “American chip products are no longer safe and reliable, and related Chinese industries will have to be cautious in purchasing American chips”. Such statements could lead to financial losses for U.S. semiconductor manufacturers by reducing their market share in China and further straining economic relations between the two nations.

China’s Export Controls and India’s Response –

China’s imposition of export restrictions on rare earth’s export is a direct response to escalating geopolitical tensions and trade restrictions by Western nations, particularly the U.S. Measures such as export controls on advanced technologies and restrictions on foreign investments have contributed to an environment of heightened strategic competition and mutual distrust. From China’s perspective, these policies are perceived as deliberate efforts to curtail its technological and economic advancement. China’s export restrictions can therefore be understood as both a retaliatory measure and a strategic counter-move. As an act of retaliation, these restrictions serve as a direct response to trade and investment limitations imposed by Western nations.

Simultaneously, as a countermeasure, China is leveraging its dominant position in the global rare earth supply chain to mitigate the economic and technological impact of the Western sanctions. REEs are subject to price volatility, and China’s export restrictions have the potential to further destabilize the market. A reduction in the availability of these critical materials could drive up costs for manufacturers, ultimately leading to higher retail prices for consumer goods that rely on rare earth, including smartphones, electric vehicles and renewable energy technologies.

For many industries, the rising costs of essential raw materials would erode the profit margins or necessitate price increases, thereby affecting end consumers. In response to China’s restrictions on critical materials, India must adopt a multifaceted strategy to enhance the resilience of its supply chains. Strengthening domestic manufacturing is a key priority, as boosting local capabilities can significantly reduce the dependency on imports. Government initiatives such as Make in India should be leveraged to foster a robust manufacturing ecosystem, enabling the country to develop self-sufficiency in key industries.

Additionally, diversifying trade partnerships is essential for securing alternative sources of critical materials.

Collaborating with technologically advanced nations such as Japan and South Korea can provide India access to high-quality components while reducing vulnerabilities associated with overreliance on a single supplier. These alliances can facilitate knowledge transfer, improve supply chain stability, and enhance India’s integration into global value chains.

Prime Minister Modi in his recent diplomatic visit to the U.S. engaged in bilateral discussions with President Donald Trump on a broad range of strategic issues, including trade, technology, defence, security, energy etc. A key outcome of the visit was the launch of the India-U.S. TRUST (Transforming the Relationship Utilizing Strategic Technology) initiative, which aims to enhance bilateral cooperation in critical and emerging technologies.

Under these initiatives, both leaders committed to strengthening trusted and resilient supply chains, particularly in semiconductors, critical materials, advanced materials and pharmaceuticals. Recognizing the strategic significance of critical materials for emerging technologies and advanced manufacturing, the United States and India agreed to accelerate collaboration in research and development while promoting investment across the entire critical mineral value chain. Both nations pledged to deepen engagement through the Mineral Security Partnership, an international framework aimed at ensuring the securing and sustainable supply of critical minerals.

Investing in R&D is another crucial element of India’s strategy. Advancing Indigenous technologies in areas such as solar panels, semiconductors, and electric vehicle (EV) batteries can reduce dependency on foreign suppliers and enhance India’s technological capabilities. By fostering innovation and promoting domestic R&D efforts, India can position itself as a competitive player in emerging industries while mitigating the risks associated with global supply chain disruptions.

Environment Challenges Related to Rare Earth Elements –

The types of REE deposits can significantly impact environmental outcomes as their processing methods differ based on the physicochemical properties of the deposits (Weng 2013). Key concerns typically include the substantial use of chemicals (such as acids and alkalis), the concentration of REEs in tailings and the presence of radioactive elements (Thorium and Uranium) in the ores. REE deposits primarily occur in four geological environments (Weng 2013; Dostal 2017): carbonatites, alkaline igneous systems, ion–ion-absorption clay deposits (predominantly in China), and monazite-bearing placer deposits.

The primary REE-containing mineral types are carbonite and alkaline igneous deposits; hence, the generation of mine tailings and the potential release of radionuclides pose significant environmental risks for REE development. REEs are mined by digging vast open pits in the ground, which can contaminate the environment and disrupt ecosystems. If poorly regulated, mining can produce wastewater ponds filled with acids, heavy metals, and radioactive material that might leak into groundwater.

The Bayan Obo stands out as the largest rare earth element mine globally, but its significance is often eclipsed by the environmental challenges posed by its tailings pond. The facility has accumulated over 70,000 tons of radioactive thorium, raising serious concerns due to the absence of adequate liners.

As a result, radioactive leachates are infiltrating the surrounding groundwater, with projections indicating that these contaminants may eventually end up in Yellow River, an essential source of potable water.

The Harvard International Review reported that the extraction of one ton of rare earth elements generates approximately 30 pounds of dust, between 9,600 and 12,000 cubic meters of waste gas – including hazardous substances like hydrofluoric acid and sulphur dioxide - 75 cubic meters of wastewater and one ton of radioactive residue. In total, this process results in around 2,000 tons of toxic waste.[1]

An effective strategy to mitigate the reliance on rare earth elements in manufacturing is for engineers and designers to create products that either minimise the usage of these elements or substitute them with alternative materials. Automotive manufacturers such as BMW and Renault have developed electric vehicles devoid of rare earth elements.

Recently, Tesla announced that its forthcoming generation of electric motors will eliminate the use of rare earth elements (REEs). Additionally, since 2017, Tesla has achieved a 25% reduction in heavy REEs in its Model 3 production. Tesla has acknowledged concerns regarding the supply chain stability and environmental impact of rare earth mineral extraction, particularly in the context of its electric vehicle production.

Colin Campbell, a member of Tesla’s powertrain executive team, presented data to investors indicating that the motors in the Tesla Model Y contain approximately 520 grams of REEs. These minerals primarily used in neodymium-based magnets are essential for generating a magnetic field strong enough to facilitate vehicular motion. In response to these challenges, Tesla introduced a next-generation permanent magnet motor that eliminates the need for rare earth elements. The company has not disclosed specific elements being removed, neodymium is believed to be the primary target, given its significant presence in Motor Y.

Researchers and industry experts have identified several potential alternatives to REEs for EVs. According to William Roberts, a senior research analyst at London-based consultancy Rho Motion, ferrite magnets composed of iron and combined with elements such as barium and strontium offer a more widely available and cost-effective alternative to rare earth-based magnets.

General Motors (GM) has previously incorporated ferrite magnets into its motor designs and in December 2023, Japan-based Proterial Ltd announced the development of motors using Ferrite magnets that matched the performance of components traditionally dependent on rare earth elements. As the demand for REE grows, there is a growing pressure to expand domestic production, which may come at the cost of environmental considerations. Governments should focus on drafting policies establishing geopolitically stable supply chains, enforcing sustainable mining and refining practices, and promoting flexibility and innovation in the use of REEs.

Emerging Players and Partnerships in REE –

As China’s dominant rare earth element (REE) reserves face depletion and emergent REE mining opportunities arise in Africa and South America, Beijing has intensified its exploratory initiatives, identifying prospective extraction sites across Southeast Asia. Presently, Malaysia, Thailand, and Vietnam occupy notable positions within the global REE supply chain.

The strategic viability of these nations as alternative suppliers is contingent upon a constellation of factors, including the magnitude and mineralogical composition of their REE deposits, their technical and infrastructural mining capabilities, and their engagement across various stages of the value chain – namely, upstream extraction, midstream processing and downstream manufacturing and end-use applications. Their ability to serve as reliable alternatives will significantly Their ability to serve as reliable alternatives will significantly depend on the coherence and competitiveness of these integrated operations.

On the production front, Vietnam mines about 600 tonnes of REE per year, but has 22 million tonnes of REE reserves- half the size of China’s reserves. Malaysia mined 80 tonnes of REE since 2024; its government has not disclosed official estimates of REE reserves but claims to have 16 million tonnes of non-radioactive REEs. These numbers suggest that while Southeast Asian countries such as Vietnam and Malaysia may have substantial reserves, their current REE production levels are significantly lower than China’s. [2]